| ECONOMICS IN CONTRACT LETTING | 347 |

|

estimated ones of the specifications, it would be hardly fair to the owner to apply to the excess those unit prices which produce his tentative limiting expenditure. Second. In the case where the actual quantities of materials are less than the estimated ones, it would be unjust to the contractor to use the high unit prices on the diminution quantities, not only because of the great difference between these and the unit actual costs, but, also, for the reason that the total overhead charges would be about the same for the dimin- ished amounts as for the estimated total quantities.

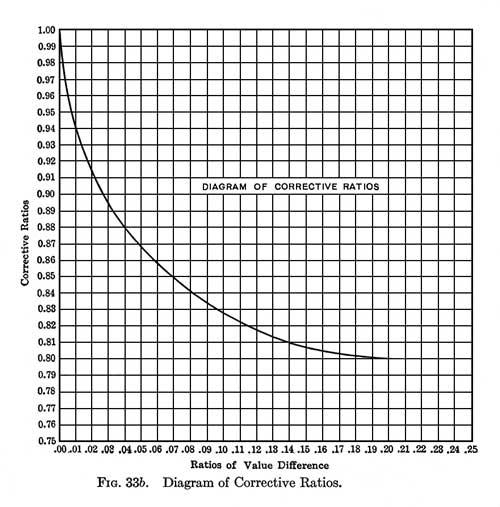

In the corrective ratio diagram (Fig. 33b) it will be noticed, that, after the ratio of value difference (due to increase or diminution of quantities of materials) reaches 0.2, the "corrective ratio" remains constant at 0.8, which corresponds approximately to actual cost conditions. The object of this is to provide that the contractor shall not be too much benefited by an abnormal increase in quantities, nor, on the other hand, shall he be at too much disadvantage because of an abnormal diminution thereof. To utilize the corrective ratio diagram (Fig. 33b) look on the line of abscissae for the ratio of cost difference, pass vertically upward to the curve (or right line, as the case may be), then horizontally to the extreme |